Retirement Calculator: Maximize Your Savings

Planning for the future can often feel like navigating a maze blindfolded. You know there is a destination, but the path is full of unpredictable variables, market fluctuations, changing tax laws, and the rising cost of living. This is where a high-quality Retirement Calculator becomes your most valuable compass.

Try our Income Tax, Mortgage, & Percentage Calculators.

Retirement Calculator

Estimate how much you may need for retirement, how your savings can grow, your retirement income gap, monthly contribution target, and a safe withdrawal plan using flexible assumptions.

Your Retirement Details

Your Retirement Result

Add your details and calculate

Your retirement readiness score and planning guidance will appear here.

Readiness: 0%

Savings Growth Chart

Retirement Income Breakdown

Detailed Retirement Breakdown

| Item | Estimated Value | What It Means |

|---|---|---|

| Click calculate to generate your retirement breakdown. | ||

Smart Retirement Planning Ideas

The more time your money has to grow, the easier it can be to reach your retirement target.

Raising your monthly savings by a small percentage every year can make a big long-term difference.

High fees can reduce long-term growth, especially over many years.

Use legal retirement accounts, pension options, and tax-advantaged plans available in your country.

By translating abstract hopes into hard numbers, a reliable retirement planning tool allows you to take control of your financial destiny. Whether you are just starting your career, aiming to retire early, or adjusting your portfolio a few years before leaving the workforce, understanding how to use these tools is the first step toward financial peace of mind.

Why You Need a Retirement Planning Tool

The fundamental question on everyone’s mind is, “how much money do i need to retire?” While a generic rule of thumb might suggest aiming for $1 million to $2 million, personal finance is deeply individual. A robust financial retirement planner takes into account your current age, income, savings, and expected lifestyle to give you a customized target.

Using a free retirement calculator can give you an immediate snapshot of your financial trajectory. By plugging in your numbers, you can determine your retirement readiness calculator score. If you find a shortfall, a retirement shortfall calculator will help you figure out exactly how much more you need to save each month to bridge the gap.

Establishing Your Baseline

Before you can effectively use a retirement savings goal calculator, you need to understand your current financial footprint. This involves using a savings estimator or retirement fund estimator to tally your current assets. A thorough retirement budget planner or retirement budget calculator will help you in estimating annual living expenses for your post-work years.

Once you have your baseline, a simple how much to save for retirement calculator or a monthly retirement savings calculator can break down your massive long-term goal into manageable, bite-sized monthly contributions.

The Core Mechanics of Retirement Projections

To truly maximize your savings, you must understand the invisible forces at play within any investment retirement calculator.

The Power of Time and Growth

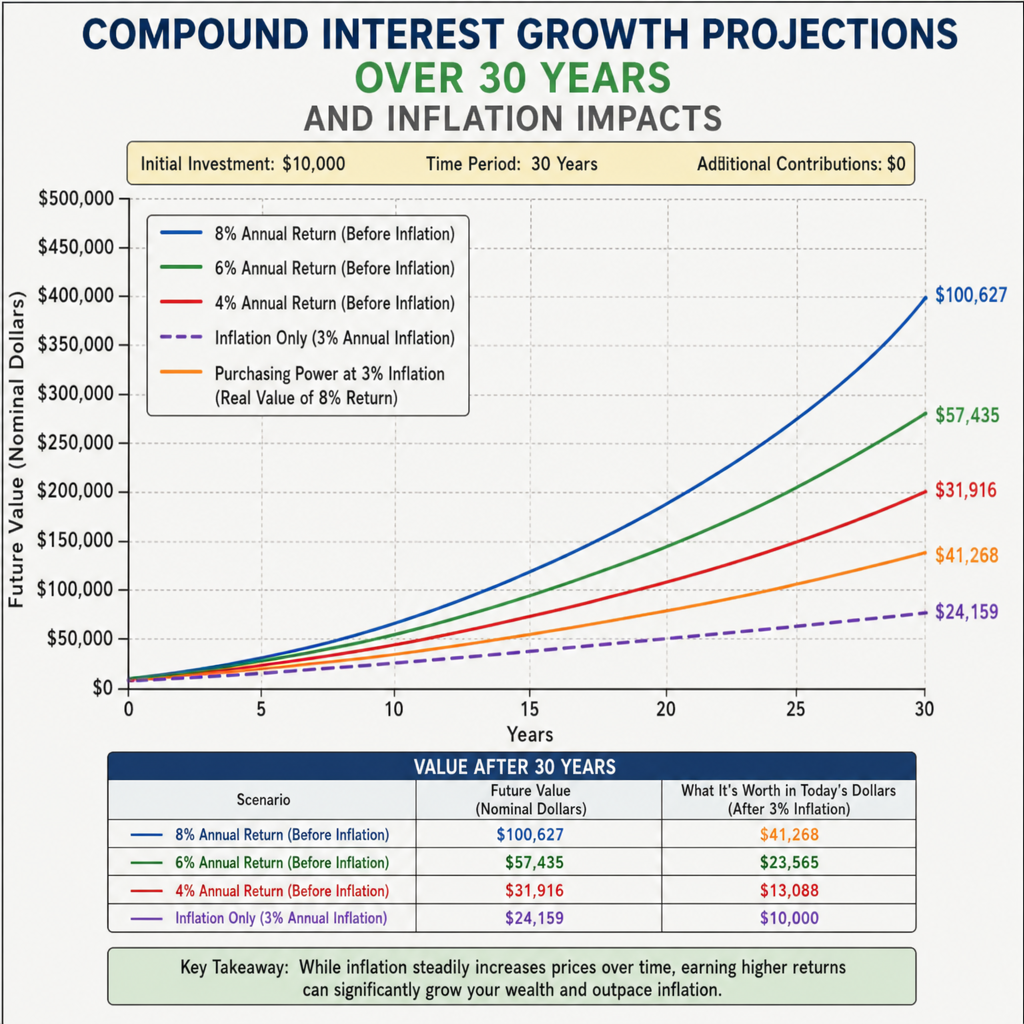

The greatest ally of any investor is time. A compound interest retirement calculator showcases the magic of compounding—where your interest earns interest over decades. Understanding compound interest growth projections can be highly motivating. Even small monthly contributions, when run through a future funds calculator, can balloon into a substantial retirement nest egg calculator output if given enough time to grow.

Battling the Silent Thief: Inflation

A million dollars today will not have the same purchasing power in twenty years. A realistic projection must include the impact of inflation on savings. Using a retirement calculator with inflation ensures that your future purchasing power is protected. If your retirement income calculator assumes a 0% inflation rate, you are setting yourself up for a severe determining future income gap.

Factoring in Market Volatility and Lifespan

Life is unpredictable, and so are the financial markets. Adjusting for investment market volatility in your retirement investment calculator by running conservative, moderate, and aggressive scenarios provides a safer baseline. Furthermore, longevity risk and life expectancy must be central to your planning. A common fear is outliving your money. Utilizing a “how long will my retirement savings last calculator” or a “how long will my money last in retirement calculator” helps alleviate this anxiety.

Navigating Employer-Sponsored Plans

For most workers, the path to financial independence runs directly through their employer’s benefits package.

The 401(k) Ecosystem

If you work in the private sector, your 401(k) is likely your primary vehicle for wealth creation. Using a 401k retirement calculator or a standard 401k calculator helps project your balance at retirement age.

- The Match: Never leave free money on the table. A 401k match calculator will show you exactly how much your employer’s contribution adds to your bottom line over time.

- Growth and Contributions: Play around with a 401k contribution calculator and a 401k growth calculator to see how increasing your contribution by just 1% or 2% can radically alter your financial future.

- Alternative Paths: If you are self-employed, a solo 401k calculator can help you maximize your unique tax advantages.

Public Sector and Non-Profit Plans

Not everyone has a 401(k). Teachers, government employees, and hospital workers often have different options:

- 403(b) Plans: Functionally similar to a 401(k) but designed for public schools and certain tax-exempt organizations. A dedicated 403b calculator will help track these specific investments.

- 457(b) Plans: Offered to state and local government employees. A 457b calculator is vital here, especially since 457(b) plans have unique early withdrawal rules that are highly favorable for early retirees.

Individual Retirement Accounts (IRAs)

Beyond workplace plans, IRAs offer incredible flexibility. A dedicated ira calculator is an essential part of your retirement savings guide.

When navigating IRAs, you must understand 401k vs ira contribution limits, as they dictate how much you can shelter from taxes each year.

- Traditional vs. Roth: The debate over tax-deferred vs tax-free income is central to retirement planning. A roth vs traditional ira calculator helps you decide whether it is better to take a tax break now (Traditional) or enjoy tax-free withdrawals later (Roth).

- Specific Calculators: Use a traditional ira calculator or a roth ira calculator depending on your chosen path. Small business owners might benefit from a sep ira calculator or a simple ira calculator to project their specialized tax-advantaged growth.

Evaluating Social Security and Pensions

Your savings are only one part of the equation. Fixed income from the government or a former employer acts as a vital safety net.

Optimizing Social Security

A standard question is, “will i have enough to retire calculator?” The answer heavily depends on your Social Security benefits. Using a retirement calculator with social security or a dedicated social security retirement calculator provides a more accurate picture of your future monthly income.

- Benefits Estimation: Proper social security benefits estimation requires looking at your earning history.

- When to Claim: A social security break even calculator (or a standard social security calculator) is crucial for deciding whether to claim benefits early at 62, at your full retirement age, or delay until 70 for maximum payouts.

Navigating Pensions

If you are lucky enough to have a pension, a pension calculator or pension projection tool is essential. Using a retirement calculator with pension data gives you a distinct advantage, lowering the total amount you need to save.

- Federal and Military: Government workers have specialized systems. A federal retirement calculator, a fers retirement calculator (or a specific retirement calculator fers employees use), and a military retirement calculator factor in years of service, rank, and high-3 average salaries.

- State and Education: Educators should look for a teacher retirement calculator or a specific calstrs retirement calculator (for California educators) to estimate their defined benefit payouts accurately.

Milestones: Using a Retirement Calculator by Age

Your priorities shift as you move through different stages of life. Searching for a retirement calculator by age or a retirement age calculator helps contextualize your current progress.

The Critical Catch-Up Years (Ages 50-55)

Hitting half a century is a major financial milestone. A retirement calculator at 50 will tell you if you are on track or if you need to utilize catch-up contributions in your IRAs and 401(k)s. By the time you use a retirement calculator at 55, your target retirement date is in clear view. This is the time to start transitioning from aggressive growth to wealth preservation.

Approaching the Finish Line (Ages 60-65)

In your sixties, the planning becomes granular.

- A retirement calculator at 60 helps you plan the exact year you intend to stop working.

- A retirement calculator at 62 is vital because it is the earliest age you can claim Social Security. You must weigh the reduced benefits against early access to the funds.

- Finally, a retirement calculator at 65 usually aligns with Medicare eligibility, making it easier to accurately project healthcare costs in financial planning.

The FIRE Movement: Rethinking Retirement

For a growing community, the traditional retirement age of 65 is simply a suggestion. The Financial Independence, Retire Early (FIRE) movement relies heavily on specialized data. An early retirement calculator or a retire early calculator operates on aggressive savings rates (often 50-70% of income) and optimized investments.

To see if this lifestyle is viable, you need a financial independence calculator or a dedicated fire calculator. The FIRE community uses early retirement fire method calculations to categorize different types of early retirement goals:

- Lean FIRE: Living on a strict, minimalist budget. A lean fire calculator will show that you need a smaller nest egg, but you must be incredibly disciplined with your retirement spending calculator.

- Fat FIRE: Retiring early without sacrificing luxury. A fat fire calculator requires massive savings and high income during working years.

- Barista FIRE: Quitting the corporate grind to work a stress-free, part-time job (often for health insurance). A barista fire calculator shows how supplemental income drastically reduces the required nest egg.

- Coast FIRE: Saving aggressively in your 20s and 30s until your investments will grow to your retirement number without adding another dime. A coast fire calculator tells you the exact day you can stop contributing to your 401(k) and “coast” to retirement age.

Turning Savings Into Income: The Withdrawal Phase

Amassing wealth is only the first half of the journey. Decumulation—spending down your assets without running out of money—is arguably more complex.

Safe Withdrawal Rates

To answer the terrifying question, “how long will my retirement savings last?” you need a retirement drawdown calculator or a retirement withdrawal calculator.

The cornerstone of this phase is the safe withdrawal rate for seniors. Most planners reference the 4% rule, which suggests you can withdraw 4% of your portfolio in year one, adjust for inflation annually, and likely not run out of money for 30 years. You can model this using a 4 percent rule calculator or a general safe withdrawal rate calculator.

Managing Taxes and RMDs

Taxes don’t stop when you retire. A retirement tax calculator helps estimate your future tax bracket. Furthermore, the IRS won’t let you keep money in tax-deferred accounts forever. Required minimum distributions explained simply: at a certain age (currently 73), you are forced to withdraw a specific percentage of your pre-tax accounts.

Failing to plan for this can result in massive tax penalties. An rmd calculator or required minimum distribution calculator is essential to foresee these mandatory withdrawals.

Guaranteed Income Strategies

If market volatility keeps you up at night, you might consider purchasing an annuity. An annuity calculator can show you how much guaranteed monthly income you can buy with a lump sum from your portfolio, acting much like a private pension.

Global Perspectives: Retirement Calculators Around the World

Financial planning is universal, but the government systems vary wildly. If you are an expat or live outside the US, you need localized tools.

Canada

Canadians rely on different pillars for retirement. A canada retirement calculator will integrate national systems. You will need a cpp calculator for the Canada Pension Plan and an oas calculator for Old Age Security benefits to get a complete picture.

United Kingdom

In the UK, the focus shifts to different terminologies. A retirement calculator uk or a pension calculator uk is necessary to factor in workplace pensions. Additionally, using a state pension calculator ensures you know exactly what the government will provide at retirement age.

Australia

Australians operate under the Superannuation system, a mandatory employer contribution scheme. To project your future wealth Down Under, you must use an australia superannuation calculator or a localized super calculator.

India

Retirement planning in India involves distinct financial vehicles. A retirement calculator india takes into account local inflation rates, which can be historically higher than in Western countries. Workers frequently use an epf retirement calculator (Employees’ Provident Fund) or an nps calculator (National Pension System) to project their tax-advantaged government-backed savings.

Evaluating Calculator Options and Methodologies

With hundreds of tools available online, choosing the right one matters.

Many people turn to well-known financial personalities and institutions. For example, a retirement calculator dave ramsey style might use a highly optimistic 10-12% annual return rate, focusing heavily on getting out of debt first. On the other hand, traditional brokerages might offer more conservative projections.

You might use a branded tool, like a myusfinance retirement calculator, or perhaps you are looking for a vanguard retirement calculator alternative with a better user interface. Regardless of the brand, the best am i on track for retirement calculator is one that allows you to customize inputs deeply—including inflation, expected returns, and changing tax rates.

For those planning alongside a spouse, a retirement calculator for couples is vital. It will sync two different incomes, two different social security payouts, and different life expectancies into one cohesive financial retirement planner.

Actionable Steps for a Bulletproof Retirement Plan

Now that you understand the terminology and the tools, how do you take action? Here is a practical retirement savings guide to implementing what these calculators teach you.

- Assess Your Current State Today: Don’t wait. Open a free retirement calculator or a comprehensive retirement planning calculator. Input your current age, salary, and savings.

- Define Your Target: Use a how much do i need to retire calculator. Ask yourself: Do I want to travel the world, or stay close to home? Adjust your estimating annual living expenses accordingly.

- Optimize Your Accounts: Check your retirement contribution calculator. Are you maxing out your employer match? Have you hit the limit on your IRA? Ensure your retirement investment calculator shows your asset allocation matches your risk tolerance.

- Run Stress Tests: Use a how long will my retirement savings last calculator and artificially lower your expected market returns while increasing expected inflation. If the future funds calculator shows you still survive, your plan is robust.

- Plan for the Inevitable: Don’t ignore healthcare costs in financial planning. Medical expenses often become the largest line item in a retiree’s budget. Furthermore, if you wish to leave an inheritance, factor legacy planning and estate goals into your end-of-life retirement fund estimator.

Overcoming Retirement Anxiety

The most common reason people avoid using a retirement savings calculator is fear. Seeing a determining future income gap or a massive retirement shortfall calculator number can be paralyzing. However, knowledge is power.

Finding out you are behind on your goals at age 40 or 50 is significantly better than finding out at age 65. If you are behind, these tools provide the exact roadmap to catch up. Whether it means adopting a barista fire calculator lifestyle later in life, working two extra years to maximize your social security benefits estimation, or simply cutting back current expenses to boost your monthly retirement savings calculator inputs, you have options.

Conclusion

Building a secure financial future does not happen by accident; it happens by design. A Retirement Calculator is not merely a digital abacus; it is a time machine that allows you to glimpse into your financial future and make necessary course corrections today.

From understanding the complexities of a 401k match calculator to navigating the intricacies of a safe withdrawal rate for seniors, utilizing these digital tools empowers you to make informed, logical decisions rather than emotional ones. Embrace the data, run your numbers regularly, and take proactive control. By carefully planning today, you ensure that your golden years are exactly that—golden, secure, and entirely on your terms.

Frequently Asked Questions

1. What is a Retirement Calculator?

A Retirement Calculator is an online tool that estimates how much money you may need for retirement based on your age, savings, contributions, expected return, inflation, retirement age, and income goal.

2. How does the Retirement Calculator work?

The calculator projects your current savings and future contributions until retirement, then compares that amount with the estimated savings needed to support your retirement income goal.

3. How much money do I need to retire?

The amount needed to retire depends on your lifestyle, retirement age, life expectancy, inflation, healthcare costs, taxes, investment returns, and other income sources such as pensions or rental income.

4. What age should I retire?

Your retirement age depends on your savings, income needs, health, career plans, pension rules, and personal goals. Retiring later can give your money more time to grow and reduce the number of years your savings must support.

5. How much should I save every month for retirement?

Your monthly retirement savings target depends on your current age, current savings, expected retirement age, desired income, investment return, and inflation. Starting earlier usually reduces the monthly amount needed.

6. What is a good retirement savings goal?

A good retirement savings goal is one that can support your expected monthly expenses throughout retirement while allowing for inflation, taxes, healthcare costs, and unexpected emergencies.

7. Does inflation affect retirement planning?

Yes, inflation can reduce the purchasing power of your money over time. A retirement calculator includes inflation to estimate how much future income you may need to maintain your lifestyle.

8. What is the 4% rule in retirement?

The 4% rule is a simple retirement planning guideline that estimates how much you may withdraw from your retirement savings each year. It is only a general rule and may not work for every country, market, or personal situation.

9. What is a safe withdrawal rate?

A safe withdrawal rate is the estimated percentage of your retirement savings that you can withdraw each year without running out of money too quickly. The right rate depends on investment returns, retirement length, inflation, and risk tolerance.

10. Should I include pension or government benefits?

Yes, if you expect pension, social security, government benefits, rental income, or business income in retirement, include them in the calculator because they can reduce the amount needed from personal savings.

11. What return rate should I use?

The return rate should match your investment style. Conservative investors may use a lower rate, while growth investors may use a higher rate with more risk. It is better to test multiple scenarios.

12. Should I include investment fees?

Yes, investment fees can reduce long-term growth. Even small annual fees may have a large impact over many years, so including fees gives a more realistic retirement estimate.

13. Does tax affect retirement income?

Yes, taxes may affect withdrawals, pensions, investment income, and retirement accounts depending on your country and account type. Always check local tax rules or speak with a qualified tax professional.

14. How can I improve my retirement plan?

You can improve your retirement plan by saving more, increasing contributions yearly, reducing debt, lowering future expenses, investing consistently, reducing fees, and using legal tax-advantaged retirement accounts where available.

15. What if I start saving late?

If you start saving late, you may need to increase monthly contributions, delay retirement, reduce retirement expenses, improve income, or use other income sources to close the retirement gap.

16. Should I pay off debt before retirement?

Paying off high-interest debt before retirement can reduce monthly expenses and improve financial security. Low-interest debt decisions depend on your cash flow, investment returns, and risk tolerance.

17. Can rental income help in retirement?

Yes, rental income, business income, dividends, or other passive income can reduce how much you need to withdraw from savings, but these income sources may also have risks, costs, and taxes.

18. How often should I update my retirement calculation?

You should update your retirement calculation at least once a year or whenever your income, savings, expenses, investment returns, retirement age, or family situation changes.

19. Is this retirement calculator accurate?

The calculator gives an estimate based on the information and assumptions you enter. Actual results may differ because investment returns, inflation, taxes, expenses, and life events can change over time.

20. Should I consult a financial adviser?

Yes, if you are making major retirement, investment, tax, pension, or withdrawal decisions, it is best to consult a qualified financial adviser or tax professional for advice based on your personal situation.