Compound interest is one of the greatest tools in personal finance it enables a modest sum saved today to grow into an immense fortune over time as you earn interest not just on its original amount but on all its interest since. Our free compound interest calculator illustrates this growth process by prompting you to enter information such as starting principal amount, annual interest rate, number of years spent accruing interest, frequency and frequency of compounding of that interest resulting in your final amount, total interest earned as well as original principal balance instantly displayed! You can go to EMI Calculator from here.

Accessing your finances clearly through numbers helps make saving and investing decisions much clearer. By testing how a higher interest rate, longer time horizon, or increased frequency of compounding affects your return, you can see why starting early is essential to long-term growth.

Compound Interest Calculator

See how your savings or investment grows over time with compound interest and regular contributions.

Year-by-year growth

How to Use this Compound Interest Calculator (CI Calculator)

This calculator takes four inputs. First, enter your Principal: the initial amount being saved or invested; enter an Annual Interest Rate as a percentage rate (for instance 7 for 7% annual return); choose Time in Years you’ll let money grow before compounding frequency – whether annual, quarterly monthly, daily – will add interest back onto balance each year or quarter; press Calculate; you will instantly see three figures: final amount earned plus interest earned with original principal referenced for comparison purposes; modify any input and recalculate to compare scenarios

What Is Compound Interest?

Compound interest is calculated based on your initial principal plus all previous interest accumulated before. Simply stated, compounding is “interest earned on money previously earned as interest”. This distinguishes compound interest from simple interest which only considers initial principals; each period’s interest added back onto your balance becomes compound interest itself; giving exponential rather than linear growth for your funds over time.

An easy way to illustrate this idea is with an example. If you invest your money at 10% per year for two years, the first year’s interest will accrue solely on your deposit; during year two you’ll see interest accruing on both elements combined – compounding rewards patience and early start more than nearly anything else when it comes to saving.

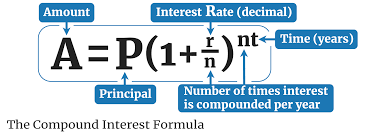

Formula for Calculating Compound Interes

The calculator utilizes a standard compound interest formula:

A = P x 1+r/n(nxt), where A is the final amount owed including principal and interest; P is your starting amount or principal amount (your starting principal amount).

R = the annual interest rate expressed as a decimal (7% = 0.07)

N = number of times interest compounds per year

At any rate of return, your interest earnings are simply A – P. An investment of Rs1,00,000 at 12% annual compounding for five years grows to about Rs1.76M with interest accruing at an approximate annual compounded rate. A similar calculation using an instant calculator yields roughly the same result – one year yielded $10550 while two and three yielded approximately the same results as calculated manually!

How Compound Frequency Affects Growth

Compounding frequency — how frequently interest is added to your balance — has an enormous effect on how much interest is accumulated. The more often interest compounds, the sooner each new payment begins accumulating its own interest. Daily compounding earns slightly more than monthly, which earns slightly more than quarterly, which earns slightly more than annual. All at the same stated rate.

There is one key distinction to keep in mind, however: as more frequent compounding becomes the norm, its benefits diminish over time. While switching from annual to monthly compounding may be noticeable, transitioning to daily compounding often only costs pennies more and can result in higher annual percentage yields on smaller balances – hence why savings accounts that compound daily often boast higher annual percentage yields (APY), but any practical differences on smaller sums is usually minimal.

The Rule of 72: A Quick Shortcut

Rule of 72 provides a quick mental shortcut for compounding. To estimate how long it will take your money to double at an annual return of 8%, divide 72 by the annual return rate – in this example it would take 9 years with an 8% rate and 12 with 6% returns respectively. Although not an exact figure, Rule of 72 gives an approximation that can quickly help you grasp how effective different interest rates may be without resorting to calculators; use it as an easy way to ensure savings or investment rates will generate meaningful growth over your time frame!

Compound Interest Works Both Ways

Compounding can be described as a two-edged sword, so it is worth understanding both aspects. While compounding can grow your savings, it also accelerates debt accumulation if interest charges add to their original balances over time. Credit cards and loans that charge compound interest can create unpaid balances which compound even faster over time, further compounding any unpaid amounts over time as interest builds upon itself. Putting off paying any compounded debt can drastically increase its total amount owed; so consistent saving from an early start and avoid carrying high interest debt to allow compounding to work for both ends! The lesson here should be clear – let compounding work to your benefit through regular savings while simultaneously avoiding high interest debt!

Compound Interest Calculator – How Money Grows

There is a reason why compound interest has been called the eighth wonder of the world. It’s that quiet power that can convert small, ordinary savings into something really impressive, with time. But for most of us the maths behind it all feels slippery, and the results can seem almost too good to be true. All of that is immediately explained on a compound interest calculator. It demonstrates exactly how an amount of money increases year after year without anyone having to wrestle with the formula by hand.

This guide explains what compound interest really is, the differences between that and the simpler kind, and how a good calculator can turn a daunting equation into a clear, motivating picture of the future. It’s for savers, new investors and anyone wondering why patience pays off so handsomely.

What is Compound Interest?

It’s a fundamental part of just about all saving and investing, and it’s worth clarifying it clearly. So what is compound interest? The simplest definition of compound interest is interest on interest. Interest earned on original amount and interest already added. In other words, the earnings start to earn too.

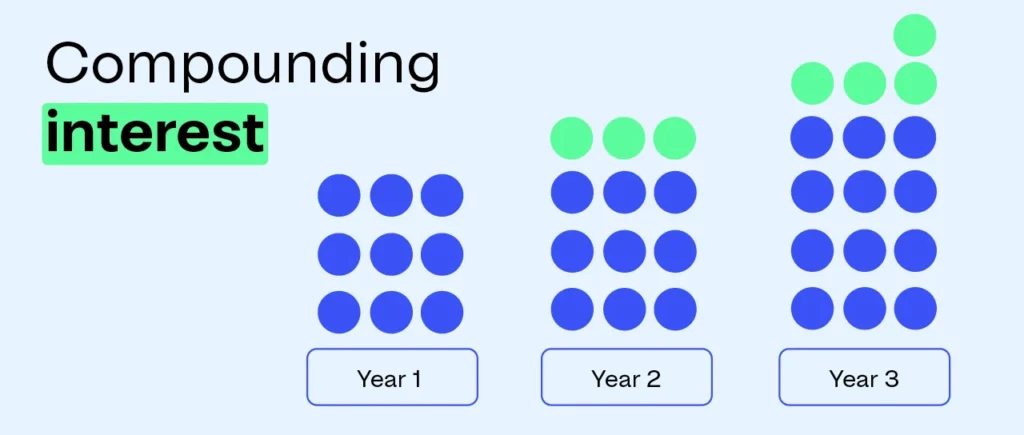

A compound is anything made of smaller parts piled on top of one another and that is exactly what happens here. You put money in, it makes interest, and that interest goes in the pot. The next round of interest is then calculated on the larger sum, so each cycle builds on the previous one. The effect is modest over a short period, but over years or decades it snowballs into remarkable growth. This is the compounding effect, which is what drives retirement funds, long-term savings and patient investing.

Compound Interest vs Simple Interest

To understand the power of compounding, it helps to contrast it with its plainer cousin. Simple interest is calculated only on the principal amount and not on the interest. The simple interest formula says take the principal times the rate times the time and that’s it, interest is flat each period.

A simple interest calculator is very handy in short-term loans and simple cases where interest does not compound. But the difference between the two methods becomes much larger with time. A deposit grows in a straight line with simple interest. It grows exponentially with compounding. The more you have the faster it grows. The longer the money is invested, the more lopsided that comparison becomes, which is exactly why compound interest has a glowing reputation.

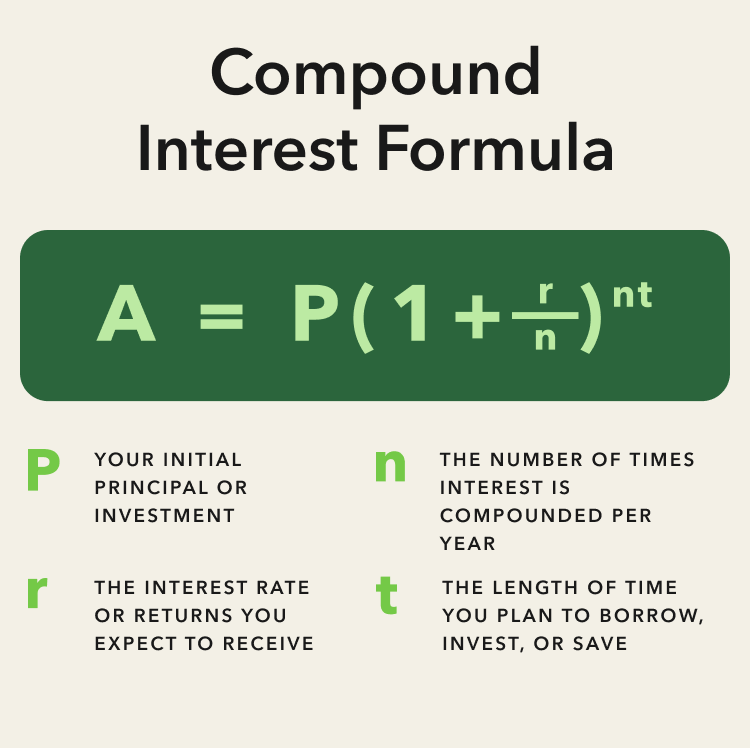

The Compound Interest Formula

If you’re the kind of person who likes to see the machinery, the compound interest formula is more approachable than it first appears. In words, the final amount is the principal times one plus the rate per period, raised to the number of periods. But it’s that tiny exponent where all the magic lies, because it’s raising a number to a higher power that gives rise to the accelerating curve.

The formula for compound interest combines four ingredients. Understanding any one of them makes it easy to trust any calculator result.

The Factors That Drive Growth

The first ingredient is the principal amount to which everything else is added. The second is the rate of interest, the percentage applied each period, which can have an outsized influence on the final figure. The third is time, the number of years you let the money grow, and it is often the most powerful lever of all because the exponent rewards patience generously. The fourth is the frequency of compounding, or how often the interest is added. The more often it happens, the more it quietly nudges the outcome higher.

A compound interest calculator simply plugs in these four values and instantly does the exponential arithmetic, saving everyone the awkward business of raising numbers to large powers by hand.

How a Compound Interest Calculator Works

A compound interest calculator is a tool that turns your four inputs into a clear projection of future value. Instead of taking a chance with the exponent, person enters the principal, the rate, the time and the compounding frequency and the answer comes out immediately. The best part is that a good compounding calculator will often break the growth down year by year so you can see the snowball rather than just an abstract number.

Given these tools have a few names. Some users want a compound calculator or CI calculator, while other users want a compounding interest calculator that takes into account regular monthly deposits, in addition to the initial sum. The engine is the same, whatever you call it, and an online version means the projection is only a few taps away. But the real value beyond convenience is motivation: seeing a balance grow on screen makes the abstract promise of long-term saving feel concrete and achievable.

How Often Interest is Added and Why It Matters

One detail that trips people up more than any other is how often interest is added. It makes a real difference. Interest can be compounded annually, quarterly, monthly, or even daily. The more often it compounds the faster a balance grows because each new slice of interest gets to start earning sooner.

This is why a daily compound interest calculator will often give a slightly higher final number than a calculator set to compound annually, even with the same rate. The one-year difference may be small, but over a long horizon those extra cycles add up. Anyone comparing savings products would do well to check the compounding frequency, not just the headline rate, as two accounts advertising the same percentage can deliver different results depending on how often they compound.

The Rule of 72

The rule of 72 is a useful mental shortcut worth knowing. To figure out how many years it takes for money to double at a certain rate, a person simply divides 72 by the interest rate. At six percent you double your money in twelve years. At nine percent, in about eight.

It is not exact, but close enough for everyday rates, and it gives a feel for the power of compounding intuitively, without any heavy calculation. A calculator will give you the exact figure, but the rule of 72 is the handy back-of-the-envelope check that makes the concept stick.

Compounding to Work: Savings and Investments

The real reason why this topic is important is that it affects how wealth is created. A savings calculator uses the same compound logic for a deposit account to estimate how a balance grows as interest compounds. A savings account calculator or savings interest calculator does this for bank deposits specifically and a savings account interest calculator can show how even a modest rate can add up over the years.

There is a higher risk with higher-yielding options. A high yield savings calculator (sometimes paired with an APY calculator or HYSA calculator) helps savers visualize the effect of a higher annual percentage yield. On the investing side, an investment calculator and investment growth calculator project how contributions might grow in the market, while a future value calculator answers the central question of what a sum today could be worth tomorrow. If you get the compounding return on investment, you can turn a vague hope into a concrete plan.

The Compound Annual Growth Rate (CAGR)

When you look back on the performance of an investment, the compound annual growth rate is the gold standard. A CAGR calculator will tell you the smooth annual rate that would have produced the actual result, but without the bumps in the road. The CAGR formula is very similar to the compound interest formula, but rearranged to solve for the rate, and it gives a fair, single figure for comparing very different investments on equal footing.

Self-Calculating Interest

The only way to build real confidence is to get your hands dirty with the numbers. The simple way to calculate interest is principal multiplied by rate multiplied by time. Compounding simply adds the application of the rate to the growing balance. If you don’t know the interest rate, the interest rate calculator can help. How to calculate interest rate per month? It’s easy! Divide the annual rate by 12 and use it monthly.

All of this ties into a larger idea known as the time value of money — the notion that a dollar today is worth more than a dollar in the future because of its ability to earn income. A calculator automates each step, but knowing the logic makes the results never a mystery.

Note About Regional Tools

Compounding is universal, but savers often want a calculator that is tuned to their own market. For instance, a compound interest calculator India edition may default to rupees and local savings conventions, while a UK edition deals with pounds and local account types. The maths is always the same, just the currency, the going rates and the nomenclature change. The best bet is to use a tool that’s configured for the right region so the numbers seem familiar and immediately useful.

Frequently Asked Questions

What does compounding mean in simple terms?

Interest on interest. You get interest on your invested money, but you also get interest on the interest you already earned. This leads to accelerating snowballing growth over time.

How is compound interest different?

Simple interest is calculated only on the original principal, resulting in a steady, straight-line growth. The longer you leave your money invested the faster the curve climbs, because compound interest is calculated on an increasing balance.

Does the frequency of compounding actually matter?

Indeed. The more often interest is added — daily instead of annually for example — the faster a balance grows, because each slice of interest starts earning sooner. The rate comparison is as important as the compounding frequency comparison.

What’s the 72 Rule?

It’s a ballpark figure for how long it takes for money to double. Divide 72 by the interest rate to get an approximate number of years, which gives a simple feel for compounding without the need for detailed maths.

Can a compound interest calculator do regular contributions?

Yes, many can. They also allow a person to add regular monthly or yearly deposits in addition to the starting principal. This is a great way to show how consistent contributions and compounding work together to accelerate growth.

Closing Thoughts

Above all, compound interest rewards two things: a good rate and, most importantly, time. Once the idea clicks – that interest earns interest and the effect accelerates the longer it runs – the appeal of starting early is clear. A compound interest calculator shows that mighty principle in action. It takes a formula with exponents and makes it into a clear story of growth, year by year. Whether you want to create a savings buffer, a retirement fund or just want to know where your money is going that clarity is the first real step in making compounding work.

What is compound interest?

Compound interest is interest earned on both your original principal and the interest already accumulated. Unlike simple interest, which only applies to the principal, compounding makes your money grow exponentially over time.

What is the compound interest formula?

A = P × (1 + r/n)^(n×t), where P is principal, r is the annual rate as a decimal, n is compounds per year, and t is years. The interest earned is A − P. This calculator applies it instantly.

How does compounding frequency change my returns?

The more often interest compounds, the more you earn at the same rate. Daily earns slightly more than monthly, which beats quarterly and annual — though the difference gets smaller at higher frequencies.

What’s the difference between simple and compound interest?

Simple interest is calculated only on the original principal, so growth is flat and linear. Compound interest is calculated on principal plus accumulated interest, so growth accelerates over time.

What is the Rule of 72?

A shortcut to estimate how long money takes to double: divide 72 by the annual interest rate. At 8%, money doubles in about 9 years. It’s an approximation for compound growth.

How can I make compound interest work harder for me?

Start early, leave the money invested longer, choose a higher rate where safe to do so, and pick more frequent compounding. Time is the biggest factor — the longer the horizon, the bigger the snowball.

Does compound interest apply to loans too?

Yes. Many loans and credit cards charge compound interest, so unpaid balances grow faster over time. Compounding can work against you on debt just as it works for you on savings.

What is APY?

Annual Percentage Yield is the real yearly rate of return once compounding is included. An account compounding daily has a slightly higher APY than the same stated rate compounded annually.

Can I use this for any currency?

Yes — the math is identical for any currency. The calculator shows a “$” symbol by default, but the result is the same whether you think in rupees, dollars, or anything else.

Is this compound interest calculator free?

Yes, completely free and unlimited, with no sign-up. Test as many principal, rate, time, and frequency combinations as you like.