An EMI Equated Monthly Installment is the fixed amount you pay your lender every month until a loan is fully repaid. Before you sign up for any home loan, car loan, personal loan, or education loan, the most important number to know is how much it will cost you each month, and how much interest you’ll pay over the life of the loan. This free EMI calculator gives you all three instantly.

Enter the loan amount, the annual interest rate, and the tenure in months. The calculator immediately shows your monthly EMI, the total amount you’ll repay, and the total interest you’ll pay on top of the principal. Knowing these figures before you visit a bank puts you in control; you can compare offers, adjust the tenure, and pick a monthly payment that actually fits your budget.

Loan & EMI Calculator

Calculate your monthly installment (EMI) for any loan — home, car, personal, business and more. Enter the asset price and down payment to auto-fill the financing amount, or just enter the loan amount directly.

Tentative Repayment Schedule

How to Use This EMI Calculator

The calculator needs three inputs. First, the loan amount is the total principal you intend to borrow. Second, the annual interest rate as a percentage (for example, enter 9 for a 9% per-year rate). Third, the loan tenure in months (a 5-year loan is 60 months, a 20-year home loan is 240 months). Press Calculate EMI, and you’ll instantly see three results: your fixed monthly EMI, the total payment across the whole tenure, and the total interest portion of that payment. Try changing the tenure or rate and recalculating it’s the fastest way to see how each factor changes your monthly burden. Check out our other calculators.

What Is an EMI?

EMI stands for Equated Monthly Installment. It is the fixed sum a borrower pays to a bank or lender on a set date each month until the loan is cleared. Every EMI is made up of two parts: a portion that goes toward the interest on the loan and a portion that goes toward repaying the principal you borrowed. Although the total monthly payment stays the same throughout the loan, the split between interest and principal shifts over time. This is known as the reducing-balance method, which is the standard used by banks and lenders.

In the early months, a larger share of each EMI goes toward interest, because interest is charged on the outstanding balance, which is highest at the start. As you keep paying, the outstanding balance shrinks, so the interest portion falls and more of each payment chips away at the principal. By the final months, almost the entire EMI is going toward principal. This is why paying off a loan early saves so much — you cut out the interest that would have accumulated on the remaining balance.

The EMI Formula

The calculator uses the standard amortizing-loan formula with monthly compounding:

EMI = [P × R × (1 + R)^N] ÷ [(1 + R)^N − 1]

Where:

- P = the principal loan amount

- R = the monthly interest rate (your annual rate divided by 12, then by 100)

- N = the loan tenure in months

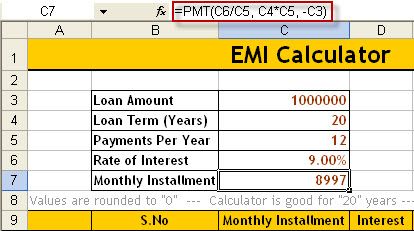

For example, take a loan of ₹10,00,000 at an annual rate of 10.5% over 120 months (10 years). The monthly rate R works out to 0.00875. Plugging the numbers into the formula gives a monthly EMI of about ₹13,493. Over the full 120 months, you’d repay roughly ₹16,19,220 in total, meaning about ₹6,19,220 of that is interest. Doing this by hand or in a spreadsheet is slow and error-prone, which is exactly why an instant calculator is so useful.

What Affects Your EMI?

Three levers control your monthly payment, and understanding them helps you structure a loan that fits your finances:

Loan amount (principal). The more you borrow, the higher your EMI and the more total interest you pay. Borrowing only what you genuinely need is the simplest way to keep payments manageable.

Interest rate. Even a small change in the rate makes a real difference over a long tenure. A home loan at 8.5% versus 9.5% can mean a meaningful gap in both your monthly EMI and your total interest, so it pays to compare lenders and negotiate.

Tenure. A longer tenure lowers your monthly EMI because the principal is spread across more months — but it increases the total interest you pay, because interest accumulates over a longer period. A shorter tenure means higher monthly payments but far less interest overall. The right balance depends on what your monthly budget can comfortably absorb.

EMI for Different Loan Types

The calculation method is identical for every fully amortizing loan, but the typical amounts, rates, and tenures differ by loan type. Home loans involve large principal amounts and long tenures, often 10 to 30 years, usually at the lowest rates because the property serves as security. Car loans are medium-sized with tenures of around 3 to 7 years. Personal loans carry higher interest rates because they’re unsecured (no collateral) and usually run 1 to 5 years. Education loans often have longer, more flexible repayment terms. Whatever the loan, you can use this single calculator; just plug in the amount, rate, and tenure that apply to your case.

Why Calculate Your EMI Before Borrowing

Knowing your EMI in advance turns a vague commitment into concrete numbers you can actually plan around. It tells you whether a loan fits your monthly budget, lets you compare offers from different lenders on equal footing, and reveals the true cost of borrowing once interest is added in. Missing EMIs has serious consequences — late fees, damage to your credit score, and in severe cases, legal action so confirming you can comfortably afford the monthly payment before you commit is one of the most important financial checks you can make.

Borrowing money is one of those grown-up milestones that can feel exciting and nerve-wracking at the same time. A home, a car, a fresh start for a small business — most big plans need a loan to get going. The part that keeps people up at night, though, is rarely the loan itself. It is the question of what the monthly payment will actually look like. That is exactly where an EMI calculator earns its place, turning a fuzzy worry into a clear, manageable number.

This guide walks through what that number means, how it is worked out, and how a simple tool can help anyone borrow with their eyes wide open. It is written for first-time borrowers and seasoned planners alike, in plain language and without the jargon that usually surrounds anything to do with loans.

What Is an EMI, Exactly?

Plenty of people use the term without ever stopping to unpack it. The EMI full form is Equated Monthly Installment, and the EMI meaning is refreshingly simple once the words are spread out. It is the fixed amount a borrower pays to a lender every month until a loan is fully cleared.

So when someone asks what is EMI, the honest answer is that it is the steady, predictable heartbeat of a loan. Each installment is the same size, month after month, which makes life far easier to plan around than a payment that jumps up and down. That single, repeating figure quietly bundles together two very different things: a slice of the original amount borrowed and a slice of the interest the lender charges for the privilege. Understanding how those two slices behave is the key to making sense of the whole arrangement.

How an EMI Calculator Works

An EMI calculator is a tool that does the heavy arithmetic so a borrower does not have to. Rather than wrestling with a long, intimidating equation, a person simply enters a few details and the answer appears almost instantly. A good loan EMI calculator asks for three things and three things only: the amount being borrowed, the interest rate, and the length of the loan.

The beauty of an online EMI calculator is not just speed, though. It is the freedom to experiment without consequences. Someone can nudge the loan amount up or down, stretch or shorten the repayment period, and watch the monthly figure shift in real time. That kind of playful testing helps a borrower discover what they can comfortably afford long before they ever sign anything. An EMI loan calculator turns a one-way decision into a sandbox, and that shift in confidence is worth a great deal.

The EMI Formula Explained

For the curious, learning how to calculate EMI by hand demystifies the whole process and makes any tool easier to trust. The EMI formula looks a little fierce at first glance, but the idea behind it is gentle enough.

In words, the formula takes the principal, multiplies it by the monthly interest rate, then adjusts that result based on how many months the loan runs. The maths is built so that the very same payment covers shrinking interest and growing principal as the months tick by. Anyone who wants to calculate EMI precisely can lean on this formula, but in practice almost everyone lets a calculator handle it, because a single typo in a hand calculation can throw the answer off completely.

Principal, Interest Rate, and Loan Tenure

Three ingredients shape every monthly payment, and getting a feel for each one is genuinely empowering.

The principal is the headline amount borrowed. A larger principal naturally means a larger installment, all else being equal. The interest rate is the cost of borrowing, expressed as a percentage, and even a small change here can move the monthly figure more than people expect. Loan tenure, the length of time taken to repay, is the sneaky one. Stretching a loan over more years shrinks each monthly payment, which feels like a win, yet it quietly increases the total interest paid across the life of the loan. A shorter tenure does the opposite: heavier monthly payments, but far less interest overall. Seeing this trade-off laid out is often the single most useful thing a calculator reveals.

Reducing Balance vs. Flat Rate Interest

Here is a detail that trips up a surprising number of borrowers, and understanding it can save real money. Interest can be charged in two very different ways.

With the reducing balance method, interest is calculated only on the amount still owed. As the principal shrinks month by month, so does the interest portion of each payment. Most modern home and personal loans work this way, and it is the fairer of the two for a borrower. The flat rate method, by contrast, charges interest on the full original amount for the entire tenure, regardless of how much has already been repaid. A flat rate can look cheaper because the headline percentage is often lower, but the effective cost is usually higher than it appears. A reliable calculator that uses the reducing balance approach gives a much truer picture of what a loan really costs.

Types of Loans an EMI Calculator Can Handle

One of the friendliest things about these tools is how flexible they are. The same underlying logic works for nearly every kind of borrowing, so a single calculator can serve many different goals.

Home Loan EMI Calculator

For most people, a property is the biggest purchase of their lives, and a home loan EMI calculator is the natural starting point. Because home loans run for many years and involve large sums, even a tiny shift in the interest rate or tenure can change the monthly payment noticeably. Testing a few scenarios here helps a buyer set a realistic budget before they fall in love with a house they cannot comfortably afford.

Car Loan EMI Calculator

A vehicle sits in the middle ground: a meaningful purchase, but with a shorter repayment window than a home. A car loan EMI calculator lets a buyer balance the dream car against a payment that still leaves room for fuel, insurance, and the occasional treat. It is a quick way to keep enthusiasm and arithmetic on speaking terms.

Personal Loan EMI Calculator

When money is needed for a wedding, a medical bill, or consolidating other debts, a personal loan often fills the gap. A personal loan EMI calculator is handy because these loans usually carry higher interest rates and shorter terms, so the monthly figure deserves a careful look. Running the numbers first helps a borrower avoid signing up for a payment that feels heavier than expected.

Bike, Business, and Education Loans

The same tool stretches comfortably across smaller and more specialized needs too. A bike loan EMI calculator suits two-wheeler purchases, a business loan EMI calculator helps entrepreneurs map out repayments against expected revenue, and an education loan EMI calculator lets students and parents plan around tuition without panic. Whatever the purpose, the calculator quietly adapts to the situation.

Reading an Amortization Schedule

Once a person knows their monthly payment, the next layer of insight comes from the amortization schedule. This is simply a month-by-month breakdown showing how each installment splits between interest and principal over the full life of the loan.

The pattern it reveals is eye-opening. In the early months, a large share of each payment goes toward interest, while only a thin slice chips away at the principal. As time passes, that balance flips, and later payments make a much bigger dent in the actual amount borrowed. Studying this schedule helps borrowers understand why paying a loan off early in its life can be so powerful, and it takes a lot of the mystery out of where the money is really going each month.

Why Prepayment Matters

Speaking of paying early, prepayment is a quiet superpower that many borrowers overlook. Whenever a person has a little extra cash, putting it toward the loan can shrink the outstanding principal ahead of schedule.

Because interest on a reducing balance loan is tied to what is still owed, a well-timed part payment lowers all the interest that would have piled up afterward. A good calculator often lets users model this, showing how a lump sum today could either trim the monthly installment or shorten the overall tenure. Even modest, occasional prepayments can add up to substantial savings over the years, which is a cheerful thought for anyone trying to get debt-free a little sooner.

The Real Benefits of Using an EMI Calculator

Beyond the obvious convenience, these tools support genuinely smarter financial planning. Knowing the monthly commitment in advance lets a borrower fit a loan neatly into a household budget rather than squeezing the budget around a surprise.

A calculator also encourages honest comparison. By testing different lenders’ rates and tenures side by side, a person can spot the option that truly costs the least over time, not just the one with the friendliest advertisement. It removes guesswork, reduces the chance of overcommitting, and gives borrowers the quiet confidence that comes from understanding their own numbers. In short, it turns borrowing from a leap of faith into an informed choice.

A Few Tips Before Taking a Loan

A little preparation goes a long way, and a handful of simple habits can make the whole experience smoother.

It helps to keep the monthly payment well within comfortable reach rather than stretching to the absolute limit, since life has a habit of throwing in unexpected expenses. Comparing offers from more than one lender is always worthwhile, because rates and terms vary more than people assume. Reading the fine print for processing fees and prepayment charges saves nasty surprises later. And running a few scenarios through a calculator before any conversation with a lender means walking in already knowing what a fair deal looks like.

Common Questions About EMIs

A few questions come up again and again, and clear answers help borrowers feel more at ease before committing.

People often wonder whether the EMI stays the same for the whole loan. On a standard fixed-rate loan, yes, the monthly installment holds steady from start to finish, which is precisely what makes budgeting so much easier. On a floating-rate loan, however, the figure can move when the underlying interest rate changes, so it pays to check which type is on offer.

Another frequent question is whether a longer tenure is a good idea. It depends entirely on the goal. A longer tenure lightens each monthly payment, which suits a tight budget, but it raises the total interest paid over the life of the loan. A shorter tenure costs more each month yet saves money overall. There is no single right answer, only the option that fits a person’s circumstances best, and a quick calculation makes that choice obvious.

Many also ask how accurate an online EMI calculator really is. For the core monthly figure, these tools are highly reliable, since the underlying maths is fixed and well established. The one caveat is that the final amount a lender quotes may include extra charges such as processing fees or insurance, which a basic calculator does not always capture. Treating the result as an excellent estimate rather than a contract is the sensible approach.

Finally, borrowers sometimes ask when the best time to use a calculator is. The simple answer is before any serious conversation with a lender. Walking in already knowing the realistic monthly commitment puts a person in a much stronger position to negotiate and to spot a deal that does not add up.

Final Thoughts

At its heart, an EMI is just a promise broken into bite-sized, manageable pieces, and an EMI calculator is the friendly tool that makes that promise easy to understand. By revealing how the principal, interest rate, and tenure interact, it hands borrowers the clarity they need to plan with confidence instead of crossing their fingers.

Whether someone is mapping out a home loan, sizing up a car loan, or weighing a personal loan, a few minutes spent with a calculator can shape a far better decision. The number that once kept people awake at night becomes something they can see, test, and steer. And that sense of control, more than anything, is what makes borrowing feel a whole lot less daunting.

FAQs

What is EMI?

EMI stands for Equated Monthly Installment the fixed amount you pay your lender every month until your loan is fully repaid. Each payment covers part interest and part principal.

How is EMI calculated?

Using the formula EMI = [P × R × (1 + R)^N] ÷ [(1 + R)^N − 1], where P is the principal, R is the monthly interest rate, and N is the number of months. This calculator applies the formula instantly.

Does a longer tenure reduce my EMI?

Yes, a longer tenure lowers your monthly EMI because the principal is spread over more months. However, you end up paying more total interest because interest accumulates for longer.

Can I use this for a home loan and a car loan

Yes. The EMI formula is the same for home, car, personal, and education loans. Just enter the relevant loan amount, interest rate, and tenure for your specific loan.

What is the reducing-balance method?

It means interest is charged on your outstanding balance, which decreases as you repay. Early EMIs are mostly interest; later EMIs are mostly principal. This is the standard method used by banks.

Why does total interest seem so high on long loans?

Because interest is charged every month on the remaining balance. The longer the loan runs, the more months of interest accumulate which is why long tenures cost much more in total even though the monthly EMI is lower.

How can I reduce the total interest I pay?

Choose a shorter tenure if your budget allows, negotiate a lower interest rate, borrow only what you need, or make prepayments when possible to cut down the outstanding principal.

Is the EMI fixed for the whole loan?

On a fixed-rate loan, yes the EMI stays the same every month. On a floating-rate loan, the EMI or tenure can change if the lender’s interest rate changes.

What happens if I miss an EMI?

Missing an EMI can trigger late-payment fees, hurt your credit score, and in serious cases lead to legal action. Always confirm you can afford the EMI before taking a loan.

Is this EMI calculator free?

Yes, completely free and unlimited. Calculate and compare as many loan scenarios as you like before you decide.